S&P500 Trading Update 15/5/26

S&P500 Trading Update 15/5/26

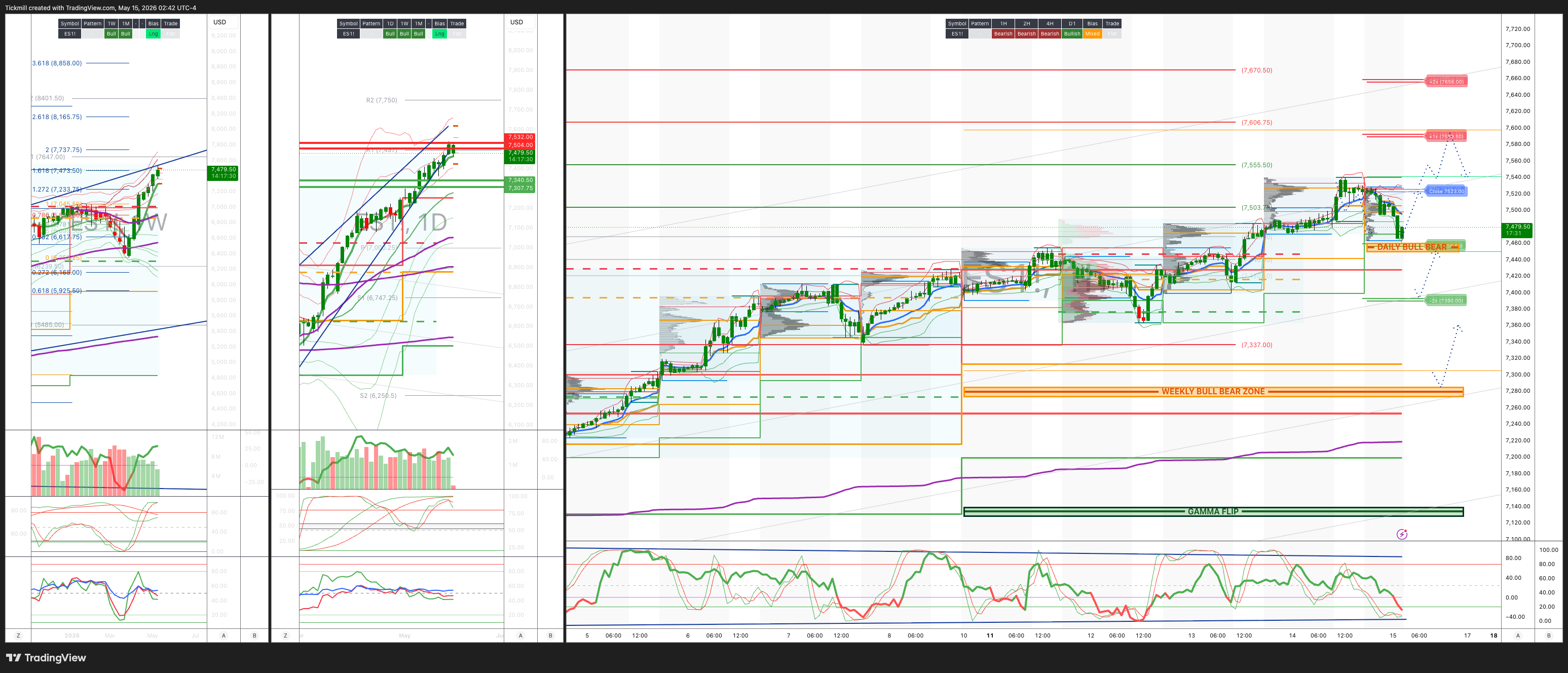

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7280/70

WEEKLY RANGE RES 7504/32 SUP 7340

May OPEX Straddle: 225pt range implies a OPEX to OPEX range of [6900, 7350]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 0.96 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7445

WEEKLY VWAP BULLISH 7255

MONTHLY VWAP BULLISH 6898

DAILY STRUCTURE – OTFH - 7479

WEEKLY STRUCTURE – OTFH - 7199

MONTHLY STRUCTURE - OTFH - 6514

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7450/60

GAMMA FLIP 7135

DELTA FLIP 6932

DAILY RANGE RES 7589 SUP 7456

2 SIGMA RES 7656 SUP 7390

VIX BULL BEAR ZONE 19.47

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET RTH/CLOSE

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Retail Participation’

Market Update: AI Leadership Reasserts, Breadth Improves, Retail Activity Rising

Markets are broadly higher as investors digest takeaways from the Trump/Xi meetings. Major US indices are moving relatively in line, with NDX +89bps, RTY +79bps, and SPX +78bps. Breadth is healthier today, with roughly 72% of S&P 500 names in the green, while the 10Y yield is cooling to 4.45% and VIX is lower by 112bps to 17.65.

The key message: the market is shifting back toward a more constructive risk tone, helped by lower yields, better breadth, and renewed AI momentum. But the speculative parts of the tape are also heating up again, especially retail favorites, bitcoin-sensitive equities, and meme baskets.

AI: still the dominant leadership engine

AI leadership remains the clearest theme. The rally was reinforced by CSCO +14% after earnings, with robust product orders led by AI and stronger guidance. That helped validate the broader AI infrastructure demand story.

Key AI moves:

AI Leaders: +180bps

AI Software: +207bps

AI Software 1-month return: +28.5%

AI Semis: +114bps

AI Semis YTD: +61.6%

The important point is that AI software is now almost back to unchanged on the year, down only -230bps, after a very sharp one-month rebound. Semis remain the standout YTD winner, up over 60%, and still appear to be the core expression of the AI capex trade.

High velocity risk is working again

The rally is not only in high-quality AI. High-velocity areas are also catching a strong bid.

Notable moves:

Bitcoin Sensitives: +450bps

Meme basket: +242bps

Retail Favorites: +29% since mid-April

This suggests risk appetite is improving, but also that the market is becoming more speculative. When AI leaders, bitcoin equities, memes, and retail favorites are all moving together, the tape is no longer just about fundamentals. Positioning, momentum, and retail participation are becoming more important.

What is not working

Some areas are lagging despite the broader rally.

Underperformers:

High Beta Momentum: -79bps

China ADRs: -295bps

MegaCap Tech vs Non-Profitable Tech: -215bps

High Beta Momentum weakness looks like some reversion after a very strong run, with the basket up 14% over the last five sessions. China ADR weakness is notable given the Trump/Xi focus, suggesting the market is not treating the meeting as a clean positive for China-linked risk.

The underperformance of mega-cap tech versus non-profitable tech also shows that the risk-on impulse is broadening into more speculative long-duration assets.

Consumer: better tone after recent weakness

Consumer news skewed more positive today. YETI +10% after solid results and commentary, while VIK +2% after better-than-expected bookings, though expectations were already higher. SN +5% is also being added to the S&P MidCap index on tomorrow’s close.

Consumer-linked baskets are seeing strong moves:

Consumer Autos: +242bps

Big Ticket Items: +274bps

Both are around +1.7 standard deviation moves

This is important because consumer discretionary has been a weak spot recently. Today’s strength does not fully reverse the bearish top-down consumer narrative, but it does suggest the group may be tactically oversold and capable of sharp rebounds when company-specific news improves.

Retail presence is becoming more important

Retail activity is rising again and is increasingly relevant for market structure.

Three key takeaways:

GIR estimates retail trading volume is up 28% since mid-April, while Retail Favorites are up 29% over the same period.

Retail activity now accounts for around 20% of total US equity trading volumes, up from 15% a decade ago, though still below the 24% peak in 2021.

Around USD 12tn of equity assets are held in self-directed brokerage accounts, equal to roughly 10% of total US corporate equity market value.

The rule changes around pattern day trading and less stringent margin requirements could further increase retail activity. That matters because retail flows can amplify momentum, especially in high-velocity areas like memes, crypto-linked equities, non-profitable tech, and AI-adjacent names.

Liquidity: improving tape quality

Liquidity continues to improve. Top-of-book liquidity is at USD 12.77 on the touch, up 10% versus the 5-day average and 27% versus the 20-day average. ETFs are 25% of the tape and continue to trend in a healthy direction.

This is a constructive market-structure point. Better liquidity makes it easier for investors to add risk and helps reduce the probability of disorderly intraday moves. That said, ETF share of volume remains high, so factor and basket flows can still dominate single-name fundamentals.

Flows: quiet but slightly mixed

Activity levels are moderate at 4 out of 10. The floor is currently skewed -1.7% for sale, but on very small notional.

Long-only investors are balanced but slightly better for sale. LO selling is most concentrated in info tech, financials, and materials, offset by demand in macro products, industrials, and communication services.

Hedge funds are +2% better to buy, led by demand in macro products, industrials, and communication services, while selling info tech, energy, consumer staples, and real estate.

The flow picture is not euphoric. The rally is being driven more by thematic momentum, better breadth, and key catalysts like CSCO than by large, broad-based institutional buying.

Trading takeaways

The market tone is improving. Lower yields, lower vol, better breadth, and strong AI leadership support the bullish case. AI remains the core leadership theme, and CSCO’s results strengthen the argument that AI infrastructure demand is real and still broadening.

However, the speculative temperature is rising. Bitcoin sensitives, memes, retail favorites, and non-profitable tech are all participating. That supports upside in the near term but also increases the risk of sharper reversals if yields rise again or if Trump/Xi takeaways disappoint.

Preferred stance:

Stay constructive on AI infrastructure and software.

Continue to own quality AI leaders, but avoid chasing the most extended semi winners.

Watch retail participation as a momentum amplifier.

Treat consumer strength as tactical unless confirmed by WMT and broader consumer data.

Be careful fading speculative risk too early while liquidity and breadth are improving.

Keep hedges in place given the market’s dependence on AI, policy headlines, and rates.

Today’s tape is healthier than recent sessions: indices are higher, breadth is better, yields are cooling, and AI leadership is reasserting. CSCO’s results provided an important validation point for the AI infrastructure cycle, while retail and high-velocity baskets show risk appetite is returning.

But this is also a market where speculative participation is rising quickly. The rally can continue if yields stay contained and AI momentum holds, but the tape is becoming more momentum-driven. The right approach remains constructive, but disciplined: stay with AI leadership, monitor retail-driven excess, and avoid overpaying for the most crowded high-beta trades.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!